Keeping your financials accurate isn’t just about closing the books on time, it’s about building trust in the numbers that drive decisions. One of the most important ways to achieve that confidence is through balance sheet reconciliation.

Balance sheet reconciliation is a critical accounting control that ensures the accuracy, completeness, and proper documentation of every balance on your balance sheet.

When performed effectively, it safeguards against errors, misstatements, and even fraud. Poor reconciliation practices, on the other hand, can leave your financials vulnerable and unreliable.

In this blog post, we’ll cover the essentials of balance sheet reconciliation: what it is, which accounts should be reconciled and how often, a step-by-step guide to the process, best practices to follow, common mistakes to avoid, and the transformative role of automation in streamlining the financial close. Let’s get started.

What Is Balance Sheet Reconciliation?

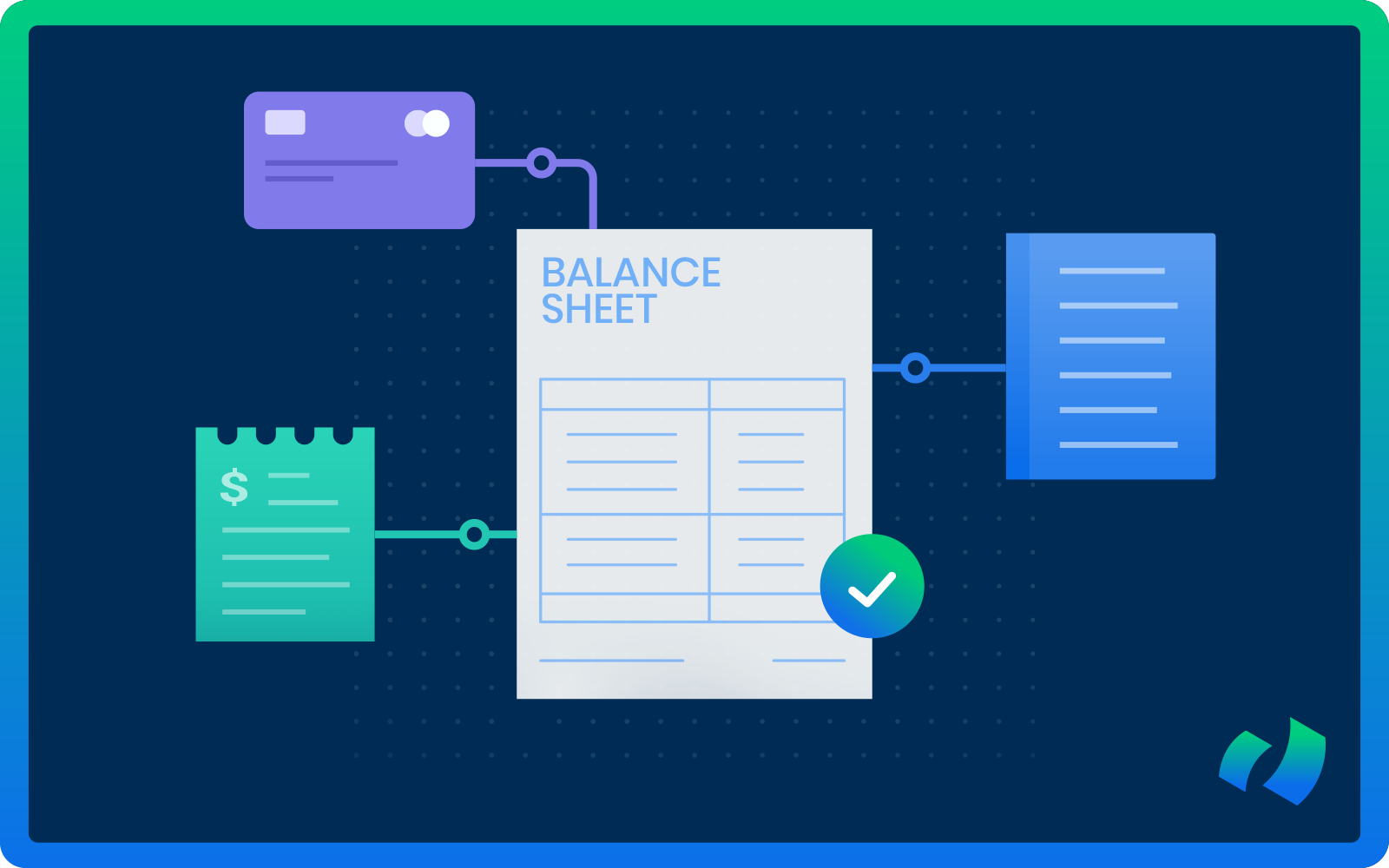

Balance sheet reconciliation is more than a month-end checkbox, it is a disciplined process of proving that each balance on the balance sheet is accurate, complete, and supported by independent evidence.

At its core, reconciliation involves tying the general ledger (GL) balance for an account to one or more reliable supporting sources (bank statements, subledgers, amortization schedules, vendor confirmations, physical inventory counts, loan statements, etc.), explaining any differences, and either clearing them or documenting an approved resolution.

The ultimate goal is to confirm accuracy, resolve discrepancies, and document results in an audit-ready format.

The Importance of Balance Sheet Reconciliation

- Enhances reliability of financial statements: Reconciliations provide the chain of evidence auditors and stakeholders depend on. When balances can be traced and explained, financial statements become more trustworthy.

- Detects errors and fraud early: Unexpected reconciling items often reveal duplicated invoices, missed cash receipts, failed data feeds, or even unauthorized withdrawals. Identifying these issues early reduces losses and remediation costs.

- Supports compliance and control frameworks: Reconciliations serve as a key control under frameworks such as SOX, IFRS/GAAP disclosure practices, and many internal audit programs. Proper sign-offs, retention of backup documentation, and segregation of duties help demonstrate control effectiveness.

- Improves management decision-making: Management depends on the balance sheet for liquidity planning, covenant compliance, valuation, and strategic choices. Clean reconciliations eliminate doubt and ensure decisions are based on facts rather than estimates.

- Reduces close-cycle time and audit friction: A consistent reconciliation routine shortens the monthly close and makes external audits faster and less expensive by ensuring evidence is organized and complete.

Balance Sheet Reconciliation Process: Step-by-Step Guide

STEP 1: Set up and assign

- List the accounts to reconcile for the period.

- Assign a preparer and a reviewer, specifying clear due dates.

- Tier accounts by materiality or risk, if needed.

STEP 2: Agree the numbers

- Compare the GL ending balance to totals from independent sources.

- Ensure any differences can be explained by reconciling items.

STEP 3: Gather and trace activity

- Pull GL balances and supporting documents (bank statements, subledgers, schedules, confirmations).

- Trace transactions—additions, disposals, receipts, payments—to source documents to verify validity and completeness.

STEP 4: Compare and classify differences

- Match GL to support totals and record differences as reconciling items.

Classify each item as:

- Timing (expected to clear naturally)

- Error (requires a correcting journal entry)

- Policy item (requires approval or write-off)

STEP 5: Correct or document

- Post journal entries for errors.

- Document timing items with expected clearance dates.

- Record approvals for policy exceptions or write-offs.

STEP 6: Document evidence

- Attach supporting materials (statements, subledger extracts, invoices, schedules).

- Record preparer and reviewer names and dates to create a complete audit trail.

STEP 7: Review and sign-off

- Reviewer verifies accuracy, classification, and supporting evidence.

- Both preparer and reviewer sign off on the reconciliation.

STEP 8: Track and close open items

- Maintain a log of reconciling items still outstanding.

- Monitor aging and escalate items that remain unresolved beyond policy thresholds.

- Clear items once evidence is available and update processes to prevent recurrence.

Which Accounts Need Reconciliation?

Not every balance sheet account requires the same level of scrutiny. Reconciliation efforts should be allocated based on materiality, transaction volume, complexity, and control risk. Prioritize accounts that move every period, are large, are susceptible to error or fraud, or feed key financial ratios.

Below is a practical, risk-based guide, including examples of typical supporting evidence.

High-Priority Reconciliations (Monthly)

These accounts are high-frequency and high-impact, so reconcile them every month.

Cash and Cash Equivalents

Verify the GL cash balance against bank statements, cleared checks, and wire receipts to identify bank errors, fraud, or timing differences.

- Support: bank statements, bank reconciliations, cancelled checks, bank confirmations.

Accounts Receivable (AR) and Allowances

Ensure accounts receivable (AR) subledger totals, unapplied receipts, and allowance estimates reconcile with the GL so that revenue and collectability are accurately stated.

- Support: AR aging, customer statements, remittance advices.

Accounts Payable (AP) and Accruals

Confirm vendor balances, unrecorded invoices, and period-end accruals are properly captured to prevent understated or misstated liabilities.

- Support: vendor statements, PO/invoice copies, accrual schedules.

Credit Card and Merchant Clearing Accounts

Match merchant deposits, chargebacks, and card fees to the GL to resolve timing differences and merchant processing exceptions.

- Support: merchant settlement reports, card statements, fee schedules.

Medium-Priority Reconciliations (Monthly or Quarterly)

These accounts often require periodic attention based on activity and materiality.

Prepaid Expenses

Tie the prepaid schedule and amortization to the GL to confirm that only the appropriate portion is recognized as expense each period.

- Support: contracts, amortization schedules.

Inventory Balances

Reconcile the perpetual inventory subledger or cycle count results to the GL to validate cost, quantities, and cost-of-goods-sold flows.

- Support: inventory counts, stock valuation reports, bills of materials.

Accrued Liabilities

Validate accrual estimates—such as payroll, utilities, and bonuses—and subsequent invoice clears to ensure accurate expense recognition.

- Support: payroll reports, accrual worksheets, vendor confirmations.

Deferred Revenue

Reconcile deferred revenue schedules and contract terms to the GL to ensure revenue recognition timing aligns with contract performance.

- Support: contract schedules, subscription/renewal reports.

Low-Priority Reconciliations (Quarterly or Annually)

These accounts typically change less frequently or are material only upon certain events.

Fixed Assets and Accumulated Depreciation

Tie the fixed-asset register, capex additions/disposals, and depreciation roll-forward to the GL to ensure PPE and accumulated depreciation are complete and correctly depreciated.

- Support: asset register, invoices, disposal paperwork.

Debt and Lease Liabilities

Reconcile loan and lease amortization schedules, payment activity, and covenant calculations to the GL to confirm principal, interest, and classification.

- Support: loan agreements, amortization schedules, lease contracts.

Equity Accounts

Verify equity movements—including capital contributions, dividends, and treasury activity—and retained earnings roll-forwards, particularly after closings and transactions affecting capital.

- Support: board minutes, stock ledgers, dividend resolutions.

Tax-Related Balances

Ensure tax payables, deferred tax assets/liabilities, and provision calculations tie to underlying tax returns and temporary differences.

- Support: tax returns, tax provision workpapers, tax authority notices.

Examples of Balance Sheet Reconciliation

Here are a few straightforward examples of how balance sheet reconciliation works in practice:

- EXAMPLE 1: Cash Reconciliation

Scenario: The GL shows a cash balance of $100,000. The bank statement shows $98,450.

Reconciling items: Outstanding checks ($1,200) and deposits in transit ($1,750).

Result: After accounting for timing differences, the adjusted bank balance matches the GL, leaving no unexplained difference.

- EXAMPLE 2: Accounts Receivable (AR) Reconciliation

Scenario: The AR subledger totals $250,000, but the GL shows $252,500.

Reconciling items: Unapplied customer payments ($1,500) and write-offs ($1,000).

Result: GL and subledger balances align after posting necessary adjustments and documenting unapplied payments.

- EXAMPLE 3: Prepaid Expenses Reconciliation

Scenario: The GL shows $12,000 in prepaid insurance. The amortization schedule indicates only $10,000 should remain at period-end.

Reconciling item: Adjust $2,000 to expense for the current period.

Result: GL now matches the supporting schedule, ensuring accurate expense recognition.

Challenges of Balance Sheet Reconciliation

Even with a clear process, balance sheet reconciliation can be challenging. These difficulties make it hard to close the books efficiently, maintain accuracy, and provide timely financial insights. Common issues include:

1) High volume of transactions

Large organizations can have thousands of transactions each period, making manual reconciliation tedious and time-consuming.

2) Human errors

Manual data entry, misclassifications, or missed invoices can create discrepancies that are difficult to detect.

3) Delayed or missing supporting documents

Bank statements, subledger extracts, or vendor confirmations may arrive late, slowing the reconciliation process.

4) Complex accounts and multiple systems

Reconciling accounts such as intercompany balances, prepaid expenses, or fixed assets across multiple systems increases complexity and risk.

5) Limited visibility and tracking

Without a central system, tracking open reconciling items, monitoring aging, or identifying recurring issues becomes difficult.

Why You Should Use Financial Close Automation Software to Reconcile Your Balance Sheet

Financial close automation software addresses the challenges above by streamlining reconciliation, improving accuracy, and increasing visibility.

Faster, more efficient reconciliations

- Automates data imports from GLs, subledgers, and bank statements.

- Reduces manual matching and repetitive tasks, freeing finance teams to focus on analysis.

Improved accuracy and reduced errors

- Automatically identifies discrepancies, duplicate entries, and unmatched transactions.

- Ensures reconciling items are properly documented and tracked.

Centralized tracking and reporting

- Monitors open reconciling items, aging, and trends from a single dashboard.

- Generates audit-ready reports quickly for management and external auditors.

Enhanced compliance and internal controls

- Enforces preparer and reviewer workflows, approvals, and retention policies.

- Supports compliance with SOX, GAAP, IFRS, and internal audit requirements.

DOKKA: A Smart Solution For Your Reconciliation

DOKKA is a leading financial close automation platform that helps teams reconcile balance sheet accounts quickly and accurately. With DOKKA, you can:

- Automatically pull and consolidate GL and subledger data.

- Use prebuilt reconciliation templates and automated matching rules.

- Track reconciling items in real time with aging and escalation alerts.

- Maintain a full audit trail, simplifying reviews and external audits.

- Reduce close-cycle time while improving confidence in financial reporting.

Implementing DOKKA allows finance teams to transform reconciliation from a time-consuming, error-prone task into a streamlined, controlled, and automated process.

Want to learn more about how DOKKA can help you? Book a demo call with our team.